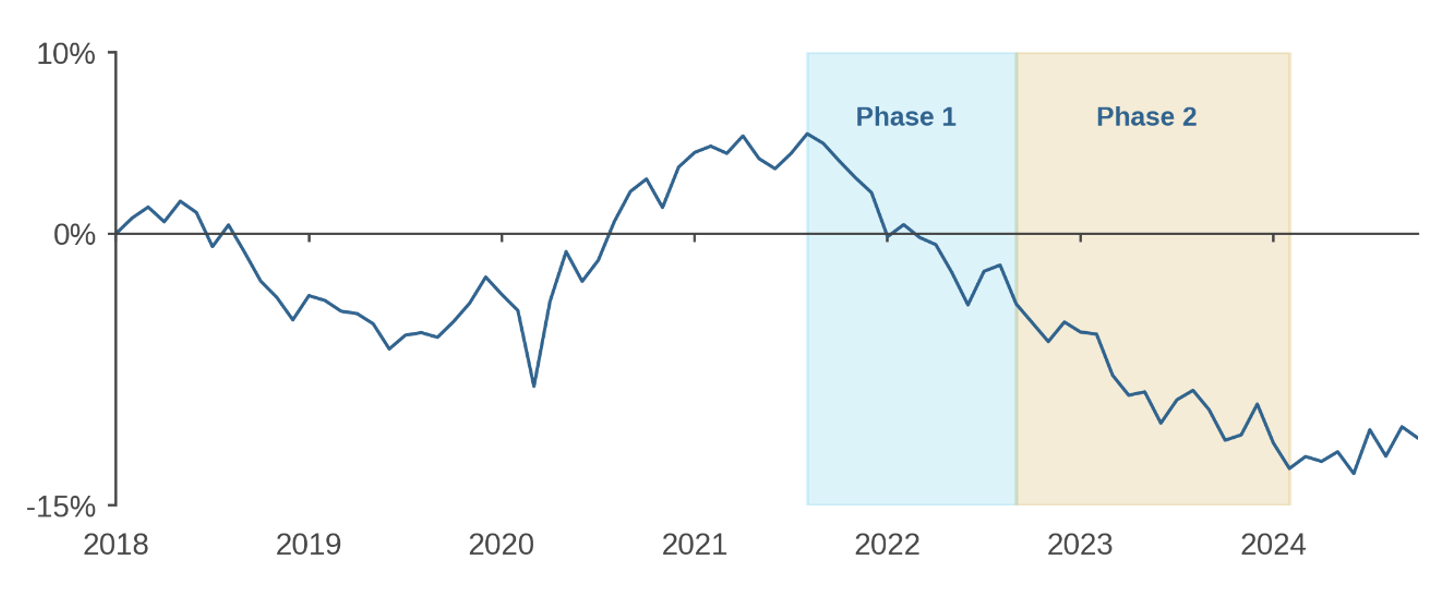

From September 2021 – February 2024, small-cap stocks in non-U.S. developed markets (DM) underperformed large caps by roughly 18% as measured by MSCI's World ex USA benchmark indexes (Figure 1). That steady relative drawdown even led some investors to question the wisdom of non-U.S. small-cap allocations. Such reflection is natural, and it can be healthy. But asset owners have a documented tendency to make ill-timed allocation decisions by overreacting to what they see in the rear-view mirror.2 Instead, we should re-evaluate non-U.S. small caps afresh.

Figure 1: Cumulative Returns – MSCI World ex-USA Small Cap Minus MSCI World ex-USA

January 2018 – October 2024

Source: Acadian based on cumulative (summed) monthly returns from MSCI. MSCI data copyright MSCI 2024, All Rights Reserved. Unpublished. PROPRIETARY TO MSCI. For illustrative purposes only. The above does not represent investment returns generated by actual trading or an actual portfolio. It is not possible to invest in any index. Hypothetical results are not indicative of actual future results. Investors have the opportunity for losses as well as profits.

This note offers such an appraisal in three parts. First, we put the recent underperformance of DM ex-U.S. small-cap stocks into broader context. While substantial, it was not historically exceptional. Next, we analyze the drawdown’s drivers, attributing it to a confluence of macro and idiosyncratic phenomena that both differ from the causes of small-cap underperformance in the U.S. and that would have been very difficult to foresee. Finally, in assessing the outlook based on valuations and expected earnings growth, we conclude that DM ex-U.S. small caps are reasonably priced relative to large caps. We believe that allocators ought to remain both invested and active in non-U.S. small caps, embracing them as an enduring source of stock-selection alpha.

Historical Context

Over the 2 ½ years from September 2021 – February 2024, DM ex-U.S. small caps significantly underperformed large (Figure 1). Figure 2 provides context for the relative drawdown, taking advantage of the long-term history available for the well-known Fama-French small-minus-big size factor (SMB).

| |

Figure 2: Fama-French SMB Factor Performance

|

|

Top chart—In DM ex-U.S., SMB’s recent slide was not unprecedented relative to the factor’s variation over its 35-year history. We see similar downturns in both the 1990s and 2000s as well as several periods of comparable relative outperformance.

|

|

|

Middle—Over the full available history since July 1990, we see no evidence of a premium to be collected simply for holding small-size exposure, per se. Even inclusive of its recent weakness, SMB has returned only -0.36% annualized with an insignificant t-stat. Moreover, net of its market beta, the factor has returned +0.03% annualized. These observations are consistent with our predisposition that small-cap exposure represents an uncompensated risk factor.

|

|

|

Bottom—Small-cap underperformance has varied around the globe. In DM, European and Japanese small caps experienced different drawdown trajectories, including variation in timing. Looking outside of DM, in emerging markets (EM), small caps have kept up with large caps over the past few years. In the sections that follow, these observations inform analysis of the causes of DM ex-U.S. small-cap underperformance as well as the outlook.

|

Data through September 2024. Source: Acadian. Based on monthly SMB factor returns from at Kenneth R. French data library (DM 3-factor, EM 5-factor). Copyright 2024 Kenneth R. French. All Rights Reserved. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit. For illustrative purposes only. |

Causes

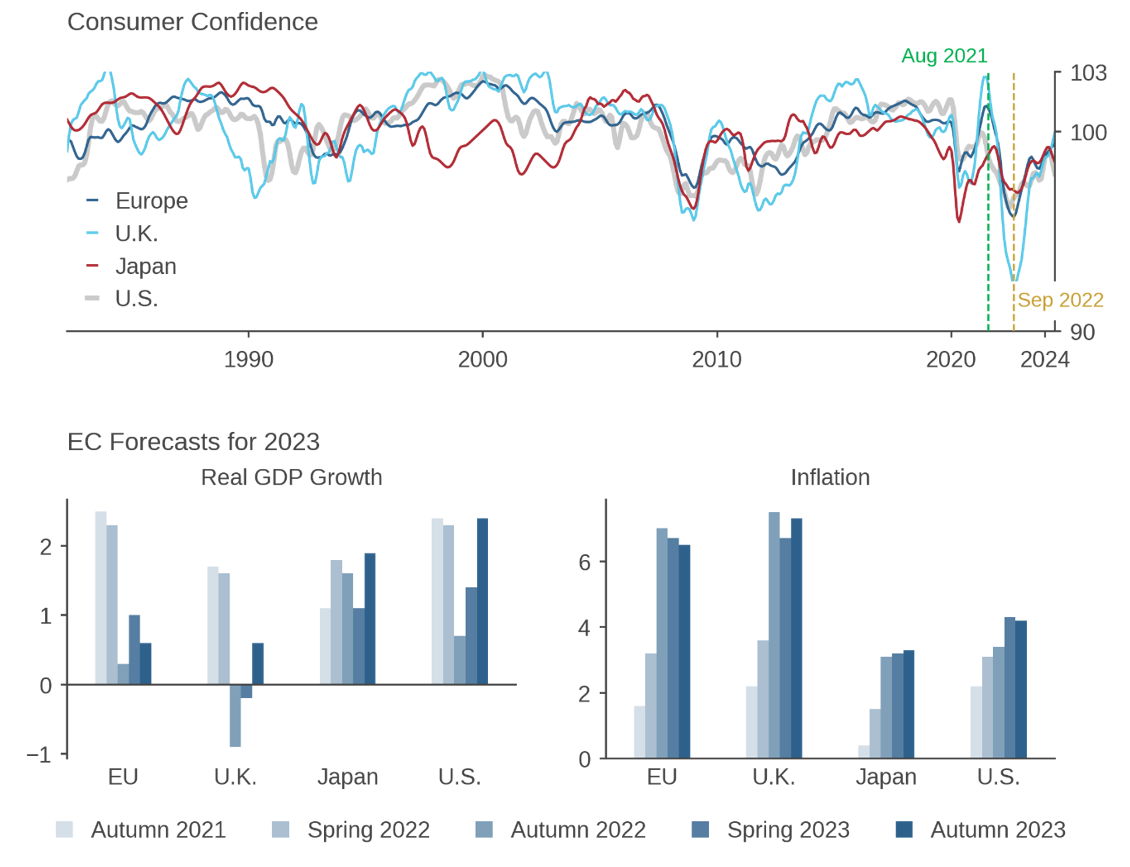

Prior to September 2021, DM ex-U.S. small-cap stocks outperformed large caps during the global speculative runup that followed the COVID selloff (Figure 1). Figure 3 offers a reminder of macro conditions that prevailed at the time. Consumer confidence was surging from COVID lows, most notably in Europe and the U.K. (top chart). Growth expectations for 2023 were healthy and inflation expectations not alarming (bottom charts).

Figure 3: The Evolution of Consumer Confidence and Economic Forecasts

Source: Acadian based on data from OECD (top chart) and the European Commission (bottom charts). For illustrative purposes only.

To understand the drivers of the subsequent underperformance of DM ex-U.S. small-cap stocks, we performed an industry-country Brinson decomposition of their performance relative to large caps. We then (subjectively) grouped both attributed and residual effects into recognizable market themes.

In our analysis, we separated the relative drawdown into two phases (highlighted in Figure 1) that were characterized by starkly different macro conditions. The first, from September 2021 – September 2022, was characterized by a global equity selloff as inflation reared its head, interest rates reset higher in much of the world, and Russia invaded Ukraine. While MSCI World ex USA dropped 27%, DM ex-U.S. small caps lost 34%.

We can attribute the lion’s share of that underperformance to four themes described in Table 1—a bid for large-cap “safe growth” in Europe as local economic conditions and sentiment deteriorated sharply, even more severe weakness in the U.K. amid successive political crises, the effects of rising interest rates, and idiosyncratic factors.3

Table 1: Key Drivers of Phase 1 Small-Cap Underperformance (Sep 2021 – Sep 2022)

|

THEME

|

IMPACT ON SMALL CAPS VERSUS LARGE

|

|

A bid for “safe growth” in Europe

In late 2021, sentiment in Europe weakened as growth and inflation expectations started to deteriorate. The bottom then fell out when Russia invaded Ukraine. (See Figure 3.)

|

- In Europe, jittery investors sought the relative stability of high-quality, growthy megacaps, i.e., firms possessing global revenue streams and solid, relatively low-volatility fundamentals. The GRANOLAS alone accounted for roughly 16% of DM ex-U.S. small-cap underperformance. 4

|

|

Acute weakness in U.K. conditions

In addition to economic worries and the war, 2022 also brought political crisis to Britain. with the collapses of the Johnson and Truss administrations. Figure 3 documents the severe deterioration in U.K. consumer confidence and economic forecasts.

|

- In the U.K., small caps were overweight consumer discretionary and industrial stocks relative to large caps, two sectors that which were punished across the size spectrum. As well, U.K. megacap energy and materials firms benefitted from rising commodity prices.5

- Within the discretionary and industrial sectors, small-cap stocks suffered larger losses than large, consistent with their greater sensitivity to the severe deterioration in local conditions.

|

|

Rising interest rates

In Q3 2021, European and Japanese interest rates started their liftoff from near zero.

|

- Relative to large-cap stocks, the sectoral composition of DM ex-U.S. small�caps left them vulnerable to rising rates. As of September 2021, the small-cap benchmark was overweight REITS (+9%) and underweight banks (-7%).

- Moreover, small-cap REITS had relatively large holdings in commercial real estate (including offices, industrials, and real estate management companies), and they were especially hard hit.

|

|

Idiosyncratic factors

Approval of GLP-1 drugs for weight-loss applications.

|

- Boosted large-cap pharma, especially Novo Nordisk, which alone accounted for about 4% of small-cap underperformance.

|

During the second phase, which started in October 2022, equity markets suddenly rebounded, yet non-U.S. small caps further extended their relative underperformance. Through February 2024, the MSCI World ex USA Index jumped 40%, while its small-cap analogue rose (only) 28%. Three themes described in Table 2 can explain of the bulk of that deficit—a recovery in lower-quality large caps, additional effects from rising interest rates (especially in Japan), and idiosyncratic effects.

We draw two inferences from the analysis summarized in the tables. First, we can largely attribute non-U.S. small-cap underperformance to transient macro risks—a confluence of economic and geopolitical phenomena— rather than to the emergence of some lasting vulnerability of small-cap companies. In the moment, the onset of an economic slowdown, generationally high inflation, the outbreak of war in Europe, and political instability in the U.K. would have been very difficult to call—and to do so faster than the market did.

Second, the causes of small-cap underperformance in the U.S. differed from its drivers in other developed markets. In contrast to the macro factors highlighted in Tables 1 and 2, in the U.S., our prior research pointed to the historical outperformance of large-cap, high-quality growth stocks (e.g., Magnificent 7) as the predominant source of relative small-cap weakness.6 The difference in drivers across regions reflects disparities in economic structures (e.g., more tech in the U.S.) and sensitivities to the specific underlying circumstances (e.g., geographical proximity to the war).

Table 2: Key Drivers of Phase 2 Small-Cap Underperformance (Oct 2022 – Feb 2024)

|

THEME

|

IMPACT ON SMALL CAPS VERSUS LARGE

|

|

A recovery in lower-quality large caps

Rebounding DM economies, lower energy prices, and expectations of government spending associated with the Ukraine war finally improved prospects for companies with weaker fundamentals, especially those that were large enough to have global revenue streams.

|

- Europe industrials alone account for roughly two-thirds of the contribution from this theme. In that sector, small caps rallied 20% but large caps jumped 50%.

- European large-cap utilities also contributed, with conspicuous gains from companies that divested Russian subsidiaries

|

|

Rising interest rates

While equity benchmarks reversed course, interest rates did not. In Europe, they drifted higher for much of 2023, and in Japan their rise accelerated.

|

- Rising rates put further pressure on REITS, resulting in small-cap underperformance through both allocation and selection effects.

|

|

Idiosyncratic factors

Continued demand for GLP-1 drugs for weight loss and waning electric vehicle demand.

|

- Novo Nordisk continued its steady rally, alone accounting for ~9% of small caps’ underperformance.

- Small-cap miners in Australia were weighed down by exposure to falling lithium and rare-earth metal prices; many lost more than 50%. This theme accounted for ~5% of the underperformance.

|

Outlook

The case for maintaining substantial non-U.S. small-cap exposure is strong. In our view, it rests on only two modest assumptions: 1) that investors ought to hold well-diversified portfolios (the cap-weighted global market portfolio being a natural starting point7) and 2) that small caps offer especially fertile ground for stock selection.

What the case does not depend on is just as important. It presumes neither that small-cap exposure offers a long-term premium nor that non-U.S. small-cap stocks currently represent a tactical allocation opportunity.

Stay Invested

Nevertheless, to play devil’s advocate, could we justify a tactical underweight in non-U.S. small caps? The most intuitive thesis would be that despite their underperformance, the market hasn’t fully priced in relative deterioration of small-cap fundamentals. But we don’t believe that to be the case. The top chart in Figure 4 shows that non-U.S. small caps are now trading at a modest P/E discount to large caps for the first time in over a decade.

Moreover, this shift in valuations is consistent with changes in analysts’ expectations of future earnings growth. While for years after the financial crisis analysts were forecasting higher earnings growth rates for small caps, the gap has been shrinking. In particular, analysts have expected more resilience from large-cap fundamentals in the face of the economic and geopolitical headwinds discussed above. As a result, the differential in short-term earnings growth expectations between small-caps and large is even tighter than it was in the shadow of COVID and the 2022 selloff, and long-term earnings growth forecasts are now in-line with one another.8 In view of current earnings expectations, we see the relative valuations of small- versus large-caps as fair.9

Stay Active

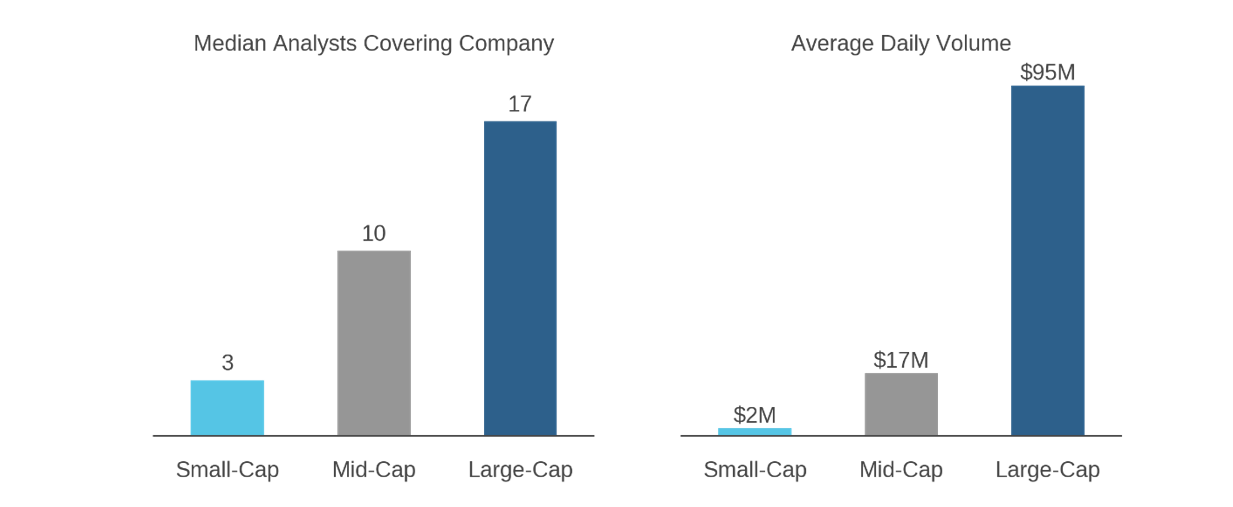

Although we do not assume that small caps offer a return premium, we believe that they offer an enduring source of stock-selection alpha. The small-cap segment’s relatively limited information environment and lower liquidity, evidenced in Figure 5, foster persistent mispricings.

|

Figure 4: DM ex-U.S. Valuations and Consensus Earnings Growth Forecasts

Source: Acadian based on index-level data from MSCI. MSCI data copyright MSCI 2024. All rights reserved. Unpublished. PROPRIETARY TO MSCI. For illustrative purposes only.

|

Figure 5: DM ex-U.S. Small Caps Versus Large—Information Environment and Liquidity

Source: Acadian. There is no guarantee that forecasts will be achieved. Hypothetical returns do not represent investment returns generated by actual trading, an actual portfolio, or an investible strategy and are not indicative of future results. Every investment program has the opportunity for loss as well as profit. For illustrative use only.

Source: Acadian. There is no guarantee that forecasts will be achieved. Hypothetical returns do not represent investment returns generated by actual trading, an actual portfolio, or an investible strategy and are not indicative of future results. Every investment program has the opportunity for loss as well as profit. For illustrative use only.

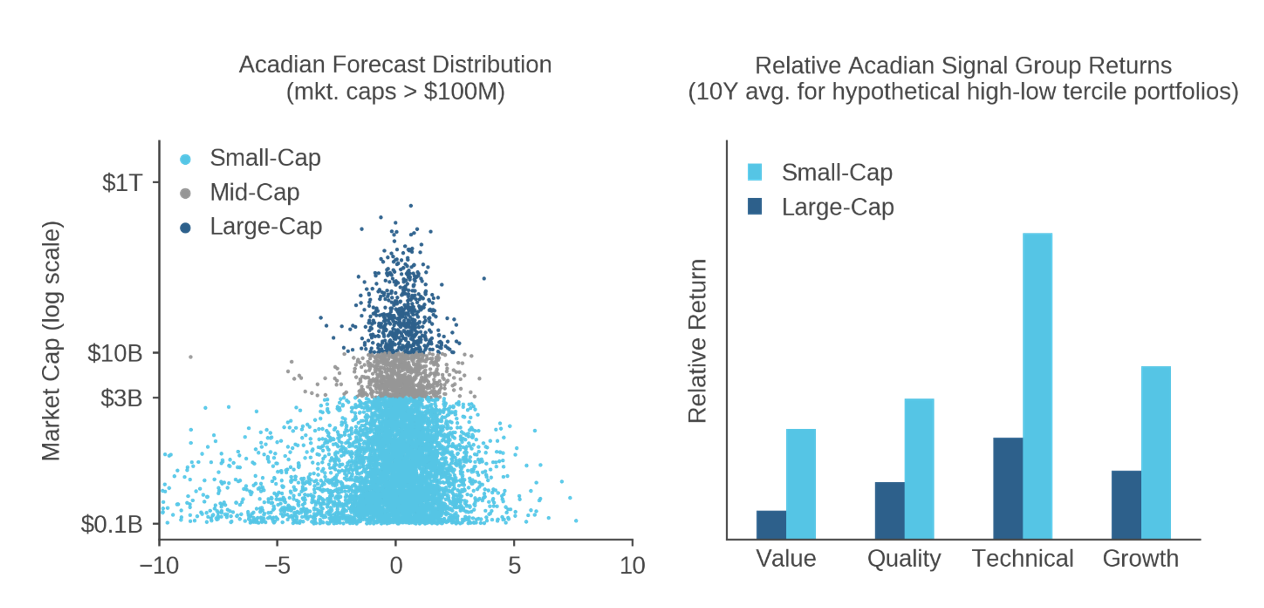

Figure 6 documents how this inefficiency benefits stock selection. The left chart shows that there is greater dispersion in our return forecasts among small caps than among large. In other words, we generally find that, on an ex ante basis, small caps look like the most attractive candidates for both overweights and underweights. The right chart then shows that the stock selection signals underlying these forecasts perform materially better in small caps than in large, ex post. These findings are not unique to the DM ex-U.S. universe—small caps offer richer stock-selection opportunities than large caps, globally.

Figure 6: Benefits of Small-Cap Inefficiency for Active Investing

Acadian DM ex-U.S. Equity Universe

Source: Acadian. There is no guarantee that forecasts will be achieved. Hypothetical returns do not represent investment returns generated by actual trading, an actual portfolio, or an investible strategy and are not indicative of future results. Every investment program has the opportunity for loss as well as profit. For illustrative use only.

What are the actionable implications for asset owners? Our prescription would depend on how the investor structures their large- and small-cap allocations. Conceptually, the cleanest long-only approach is to pool them into a single all-cap active allocation. To the extent that alpha dispersion is generally higher among small caps, such a portfolio will naturally tend to overweight small-cap stocks relative to the market portfolio. In the absence of a binding risk constraint on size exposure, the degree of that overweight can fluctuate as the forecasted opportunity set for stock selection among small caps expands or contracts relative to large caps.10

The pooled allocation framework clarifies the prescription for investors who instead separately allocate to large and small strategies in DM ex-U.S. (and other regions). First, stay active in small caps because that’s where the stock selection opportunity set is richest. Second, as a general rule, overweight active small caps relative to large. The degree of that small-cap overweight should depend on investor-specific views and constraints, including expectations of small-cap alpha and tolerance for small-cap risk.11

Conclusion

In our view, it would be understandable but unwise for institutional investors to reduce their allocations to small caps in non-U.S. developed markets based on their performance over the past few years. Currently, we think that these stocks, in aggregate, look reasonably priced relative to larger caps. Over the long run, we would encourage allocators to view small-cap exposure as an uncompensated risk factor that is well worth taking to exploit stock-selection opportunities in a relatively inefficient segment of the market. Based on a forward-looking perspective, stay both invested and active in non-U.S. small caps.