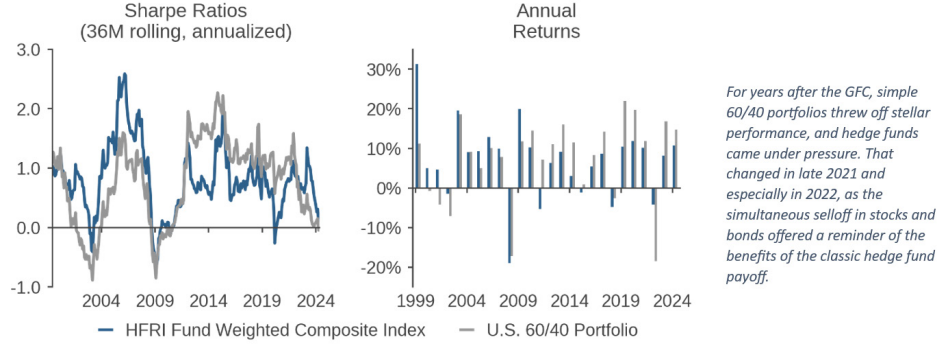

For years after the GFC, hedge funds gradually lost favor with asset owners as interest rates fell and equity markets marched steadily higher. Whether a fair comparison or not, the performance of traditional 60/40 portfolios was hard to beat (Figure 1). In that environment, investors put pressure on hedge fund fees, and there was media discussion as to the viability of the asset class.1 The picture changed markedly in 2022 as speculative froth ebbed and stocks fell sharply. Bonds, which for many years had provided a reliable cushion in times of market stress, became highly correlated with stocks as inflation surged. In those difficult market conditions, hedge funds outperformed and breathed new life.

Figure 1: Hedge Fund Performance Versus 60/40

1999 – May 2024

Source: Acadian based on HFRI index data from Bloomberg and U.S. equity market returns from the Kenneth R. French data library (Copyright 2024 Kenneth R. French. All Rights Reserved.). The chart represents an educational, illustrative exhibit and does not represent investment returns generated by actual trading or actual portfolios. Results do not represent the returns of investible strategies. They do not include trading costs, borrow costs, and other implementation frictions. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

That recent experience reinforced the compelling premise of hedge fund investing: a strategy that offers positive excess returns with little co-movement to major asset classes should be of great value to asset owners. The problem for allocators has long been how to find one. That task grew enormously complicated over the past twenty years as the number of hedge funds exploded. It also grew risky, as so many of those expensive investments delivered disappointing results.

In this note, we consider the hedge fund allocator’s challenge afresh. The first section reviews the advantages of a multi-strategy vehicle in building a hedge fund allocation (skippable by readers who are already familiar with the arguments). We then compare two operating models for a multi-strategy hedge fund. The second section evaluates the outlook for what has become the dominant paradigm, the multi-manager platform, highlighting questions around its generalizability and durability. The final section considers advantages of a rising challenger, the integrated systematic multi-strategy model, with respect to cost, risk management, transparency, and liquidity.

Multi-Strategy Hedge Funds: Reiterating the Case

THE HEDGE FUND VALUE PROPOSITION

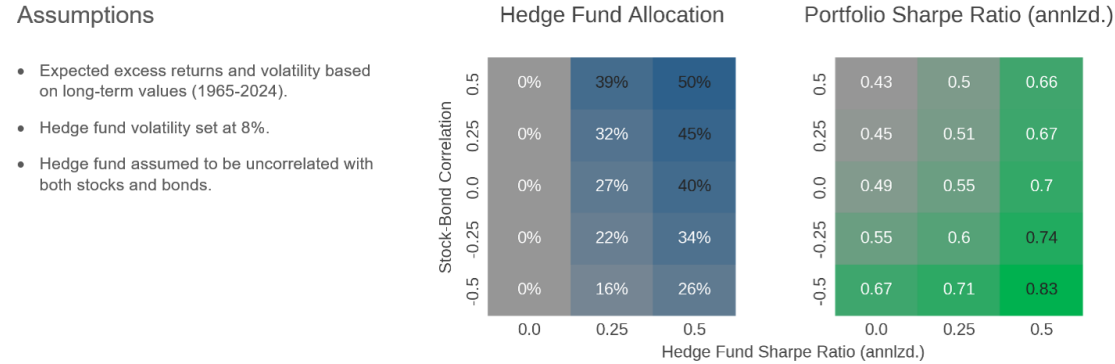

There is a compelling case for an allocation to the canonical hedge fund: an investment with positive expected excess returns (versus the risk free rate) that are unrelated to those of major asset classes.2

Figure 2 reinforces both the evergreen case for hedge funds and their timely appeal in the current investing climate. In a hypothetical exercise based on historical equity and fixed income performance, the heatmap shows that a strategy offering classic hedge fund returns would warrant a material allocation, even if it were expected to deliver a modest positive Sharpe Ratio. In a climate of correlated stock and bond returns, like that observed in recent years, the optimal allocation grows larger because the hedge fund’s diversification benefit increases.

Figure 2: The Case for an Uncorrelated Hedge Fund Strategy

Sharpe Ratio-maximizing allocation to a hypothetical hedge fund alongside stocks and bonds

Source: Acadian. For illustrative purposes only.

BENEFITS OF A DIVERSIFIED HEDGE FUND ALLOCATION

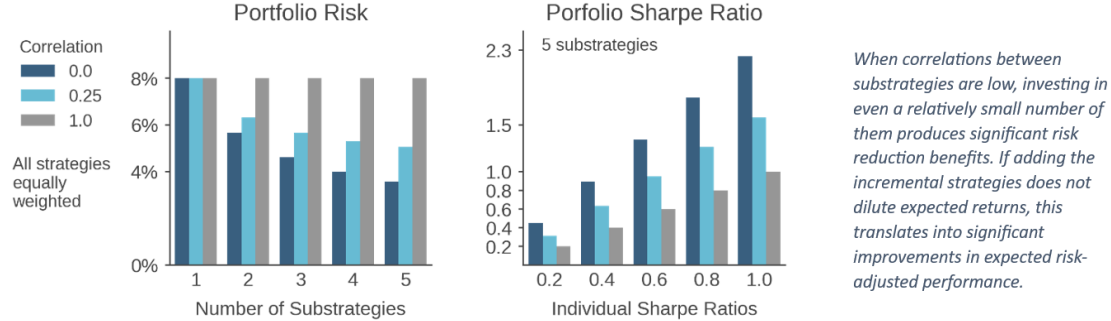

To deliver these ideal attributes, it makes sense to diversify across several hedge fund strategies that have distinct performance drivers and produce largely uncorrelated return streams.3 Along with greater capacity, anticipated benefits, including reduced volatility, less lumpy payoffs, and smaller drawdowns, would improve expected risk-adjusted performance—as long as adding incremental strategies is not overly dilutive to expected returns. The left panel of Figure 3 shows that aggregating even a small number of substrategies achieves significant diversification benefits—if they are truly orthogonal. The right panel illustrates the benefit in another way, showing that a small set of distinct hedge fund strategies with individually modest Sharpe Ratios can be combined to generate much stronger risk-adjusted performance.4

Figure 3: Diversification Benefits of Hypothetical Uncorrelated Substrategies

Source: Acadian. For illustrative purposes only.

Advantages of a multi-strategy hedge fund

In assembling a diversified hedge fund portfolio, asset owners can go it alone or outsource the task. For many, a multi-strategy hedge fund vehicle offers advantages that make the latter route preferable. Some derive from consolidation of the asset owner’s burden with respect to manager selection. Similar to a fund of funds (FOF), the single multi-strategy entity relieves the asset owner of the burden of selecting and sizing several substrategies, and it may have access to a superior pool of investments and better resources with which to accomplish the task. A multi-strategy fund should also be more capital efficient than a collection of individual hedge fund allocations or a FOF, being able to exploit natural risk offsets across its entire portfolio in taking leverage.

A multi-strategy fund should also offer cost advantages. They include operating efficiencies, for example the consolidation of administrative and execution functions as well as, perhaps, data and analytical resources. Another may be fee netting. With a classic 2-and-20 fee model, the multi-strategy fund would base the 20% performance fee on the portfolio’s composite payoff. Mathematically, this amount would be less than or equal to the sum of equal performance fees applied to the individual substrategies. That’s because only in the multi-strategy case does negative performance from any substrategy offset positive contributions to fees from other substrategies. In fact, an investor who holds a basket of individual hedge funds may wind up paying performance fees even if their return on the aggregate allocation is negative. Figure 4 illustrates that all other things being equal, the better diversified the substrategies, i.e., the less positively correlated they are, the more consequential performance fee netting becomes. From the subjective perspective of the investor, the expected magnitude of fee netting diminishes as their expectation of alpha from the sub-strategies rises relative to risk (across dark blue to light blue columns), since performance offsets would be less likely.5

Figure 4: Performance Fee Netting Illustration — Hypothetical Multi-Strategy Hedge Fund

Estimate of fee netting over one year as a function of substrategy diversification and expected alpha

Key assumptions include: Investor expects that strategy returns are normally distributed and alpha accrues at a constant, continuous rate; volatility is expressed in continuous time; there is no management fee, hurdle rate, or high water mark; investor cannot redeem within one year. Source: Acadian. For illustrative purposes only.

A multi-strategy fund also offers advantages in risk management. Multi-strategy funds require a centralized function to govern final portfolio construction. It assigns capital and risk tolerances to each substrategy and may hedge out excess risk exposures in the aggregate portfolio. In a multi-strategy fund, this function should have greater visibility and control than an LP or FOF overseeing a portfolio of external investments. It should have full transparency into each component portfolio in real time, which, among other benefits, unlocks the value of sophisticated portfolio construction methods.6 As well, if the investing climate changes, a multi-strategy manager should be able to reallocate or reduce risk across substrategies as quickly as underlying instruments can be traded; it faces no lockups, gates, or other frictions that hedge funds impose on external investors.

In summary, there are many reasons for hedge fund investors to embrace the multi-strategy concept.

The Multi-Manager Model: Limits?

RISE TO PROMINENCE

Increased interest in multi-strategy hedge funds has been intertwined with ascendence of the multi-manager hedge fund structure. (See the sidebar glossary.) Multi-manager platforms, “now a dominant force in the industry,”7 account for the vast majority of hedge fund AUM growth in recent years.8 Their rise reflects strong aggregate performance. A recent Barclays analysis, for example, reported that aggregate returns and alphas posted by multi-manager funds have exceeded those of the broader hedge fund industry over the past five years.9

The multi-manager structure can be viewed as a pragmatic compromise in aggregating siloed investment processes. It preserves decentralized decision making by specialist PM teams with respect to trade analysis, sizing, and timing, while generating benefits from consolidation in other parts of the investment process. While the multi-manager structure can be applied to create a single-strategy hedge fund, e.g., long-short equity, it is most associated with the multi-strategy context.

QUESTIONING THE DOMINANT PARADIGM

Despite the intuitive motivation and perceived success of the multi-manager structure, there are reasons to question whether it is a generalizable and durable operating paradigm. Asset owners may find it a fool’s errand to chase the past performance of the most prominent such platforms. Many of them are closed to new money,10 and their success has been hard for other firms to replicate. Across the space, industry research reveals considerable dispersion and recent softness in multi-manager performance.11

The multi-manager model also faces cost pressures arising from its decentralized premise. The individual PMs acquired by or contracted to the platforms typically view themselves as independent free agents, and they are compensated based on their standalone performance rather than the fund’s composite return. While dominant multi-manager platforms have ready capital and other non-pecuniary resources to attract talent, sought-after PMs create bidding pressure for their services.12 In contrast to free-agent models found in many professional sports, where team owners protect their interests as investors, imposing salary caps and other devices to limit aggregate costs of bidding, hedge fund LPs have no such protections. In an industry hallmarked by opacity and information asymmetry, the risk is high that some multi-manager firms will overpay.

In addition, buildouts of multi-manager platforms have been expensive. Industry research has highlighted that since 2015, the fraction of their headcount in non-investment roles has risen from 40% to 54%.13 Staff, data, and analytical resources may not be fully sharable across compartmentalized PMs, perhaps limiting gains in operating efficiencies from centralization. The multi-manager compensation model exacerbates rigidities. Because PMs are paid based on their own performance rather than the fund’s return, they are incentivized to jealously guard their resources and analysis. They may demand a larger cut of their profits to share them.

Ultimately, it is the end investors in the multi-manager funds who bear these costs. They may manifest in the form of “pass-through” fees, which have become the norm in the multi-manager space. Pass-through fees replace the fixed management fee of the classic 2-and-20 model with a variable charge. They allow platform managers to charge LPs for whatever expenses they incur, including compensation. As a result, they may reverse benefits of fee netting, which are a key attraction of the multi-strategy concept. Pass-through fees are significant, according to some sources averaging roughly 5% of AUM among firms that levy them but sometimes far exceeding that amount.14

As a result of these factors, the fraction of returns captured by multi-manager investors has dropped materially, and, by one estimate, now stands at only $0.41 per dollar of performance generated.15

A Systematic Multi-Strategy Fund: A Better Alternative?

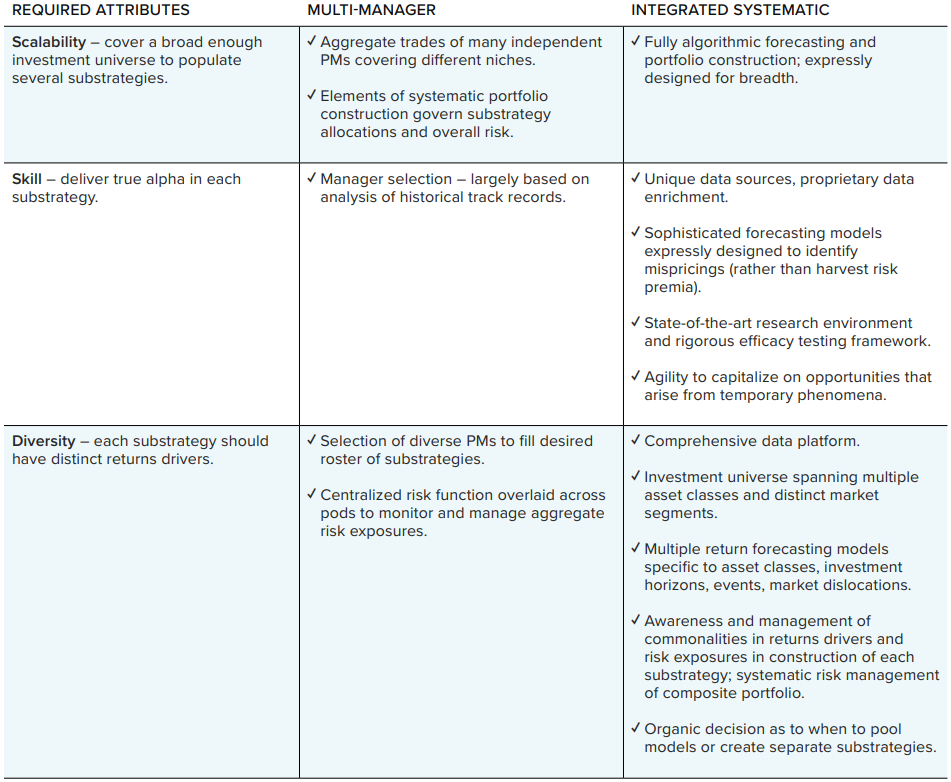

As a foundation for a robust multi-strategy offering, the operating model for a hedge fund should possess three attributes: scalability, skill, and heterogeneity. Figure 5 motivates these characteristics and contrasts how they are supplied by the dominant multi-manager operating model to a rising challenger, the systematic multi-strategy hedge fund. This alternative structure is a vehicle that contains several distinct systematic hedge fund substrategies, each born from an integrated research and efficacy testing platform, that are combined and risk managed via systematic portfolio construction methods.

Figure 5: Contrast of Multi-Strategy Hedge Funds—Multi-Manager Versus Integrated Systematic

As noted in the table, not just any systematic investing approach will deliver the sufficient skill and diversity to drive a multi-strategy hedge fund. Key attributes include a data platform that is broad enough to support investment decision making in diverse contexts and that contributes to skill by offering unique data sources and proprietary enrichments. Forecasting models should reflect both the intent and analytical sophistication to distinguish alpha from risk, and they should be validated by rigorous and exhaustive efficacy testing.16 To ensure that they can support diverse substrategies, predictive models should be specialized for distinct contexts (such as asset classes, market segments, or investment horizons) and special market circumstances, even though they are developed in a consistent analytical framework and leverage sharable intuition, methods, data, and even signals. The investing philosophy and process should be flexible enough that they can be applied to capitalize on opportunities that arise from temporary phenomena.

So constructed, an integrated systematic multi-strategy fund offers several advantages:

Cost: The systematic approach naturally reduces cost pressures associated with the decentralized multi-manager structure. First, it better aligns incentives of manager and investors. As a collaborative enterprise, a systematic investing platform does not face the dissonance created by bidding for free-agent talent based on their standalone performance when LPs are receiving a composite returns stream. Second, systematic investment processes, by nature, are designed to scale, thus providing a more natural basis to cover broad investment universes required to populate robust multi-strategy funds than the narrow and resource-intensive discretionary investing approaches that are so closely identified with pod structures. Third, compared to a more compartmentalized multi-manager structure, we would expect greater cost efficiencies from an integrated research and efficacy testing environment where, from the outset, data and analytical infrastructure and resources are designed for maximal breadth and flexibility of use.

Transparency: That the investment process of a systematic multi-strategy offering is fully codified ex ante lends far greater transparency in performance analysis than is typical in hedge fund contexts. So does the shared research environment at the heart of an integrated systematic platform. In contrast, opacity is a particular concern in pod structures. It is no easy task, for example, to develop a coherent picture of performance drivers across disparate discretionary investing approaches managed by PMs who are incentivized to guard their IP.

Risk management: The multi-strategy premise hinges on diversification across substrategies. But decentralized decision-making raises the risk of commonalities in return drivers and risk exposures. These vulnerabilities can be subtle, and the multi-manager model’s defenses against them—prudent manager selection and a centralized risk function—are incomplete. Insidious risks, including non-linear downside market exposure, may originate deep within seemingly distinct investment approaches, and they may be too rare or transient to detect in available manager track records.17

A systematic approach and a common research environment offer a manager unrivaled tools not just to surveil diversification ex post, but to engineer it from the outset. In risk and performance analysis, full knowledge of signal and portfolio construction (not just current portfolio composition or simply a returns history), provides invaluable insight to distinguish emerging patterns from noise and allows the application of much more data-intensive and informative diagnostics. Moreover, in designing a new model, a manager can explicitly minimize overlap with existing strategies through signal selection, nuanced signal construction, exposure guardrails, or even formally orthogonolizing the model's forecasts against others.

Liquidity: Generally speaking, systematic approaches maximize edge through breadth, i.e., by spreading independent “bets” across an expansive investment universe and over time. To do so, portfolio construction involves careful modeling of trading costs and position sizing relative to available liquidity on both the long and short sides. Given this approach, a systematic multi-strategy fund may be able to offer investors a high degree of liquidity, on the order of days or weeks, not months or years, and specific liquidity requirements can be “baked into” portfolio construction of the individual substrategies (even influencing signal selection). In an environment in which some multi-manager hedge funds have extended lockups beyond two years and many private market investors are starved of distributions, liquidity in a multi-strategy hedge fund certainly would be welcome. To paraphrase one asset owner, “A diversifying strategy loses appeal if you can’t tap it for liquidity when you need to rebalance.”

Conclusion

As a foundation for a robust multi-strategy hedge fund, an integrated systematic investing platform offers an intriguing alternative to the dominant multi-manager paradigm. While an integrated core might seem inconsistent with the concept of driving several distinct substrategies, a well-designed systematic platform can deliver the informational breadth, skill, and contextual diversity to address the challenge. In summary, the returns stream classically associated with a multi-strategy hedge fund investment should be of great value to investors, and in delivering it a systematic approach offers unexpected advantages, among them cost, risk, transparency, and liquidity.

A PRACTICAL HEDGE FUND GLOSSARY

Hedge fund: A pooled investment vehicle seeking to generate positive absolute returns that are unrelated to those of major asset classes.

Fund-of-funds: An entity that invests in other hedge funds. Assumes the responsibility of manager selection from the asset owner (for an additional fee).

Multi-strategy hedge fund: A single investment that delivers a composite returns stream generated by diversifying across multiple hedge fund substrategies. Substrategies may be developed in-house, hired in, or contracted to a third-party provider. Performance fees are assessed based on the composite returns stream, hence may provide benefits of fee netting.

Pass-through fees: A fee structure that has become highly prevalent in the multi-strategy world, although it is also applied to single-strategy funds, by which managers can pass along all kinds of expenses, including compensation costs, to investors. Pass-through fees fully/partly replace the traditional fixed management fee and, in the multi-strategy context, can unwind benefits of fee netting.

Multi-manager (a.k.a. multi-pod) hedge fund platform: A hedge fund operating model in which a centralized mechanism allocates capital to multiple autonomous investment decision makers. The structure can support both single- and multi-strategy hedge funds. Pods may be in-house or outsourced and may represent anything from a discretionary stock picker covering a narrow niche to a standalone hedge fund strategy (e.g., L/S equity, macro, convert arb, special situations, etc.).

Integrated systematic multi-strategy platform: A hedge fund operating model in which a shared research framework is applied to form a number of distinct systematic hedge fund substrategies that are combined into a multi-strategy fund using systematic portfolio construction.

|