September 2018

Despite the wave of headlines devoted to the “rise of passive,” the trend’s effects on market behavior remain poorly understood. That ambiguity has further fueled the hype by preserving the plausibility of provocative yet unproven narratives, including warnings of valuation distortions due to robotic flows into passive vehicles, rationalizations of stock pickers’ poor performance, and even proclamations of the impending death of active management.

As a quantitative active manager, we have natural interest in understanding how passive investing may affect our opportunity set and the efficacy of our signals. In this note, we lay out competing hypotheses about passive’s effects based on two contrasting assumptions regarding the source of passive flows. We evaluate them by exploiting cross-sectional variation in stocks’ passive ownership.

We find evidence that passive investing is modestly reducing the short-term efficacy of active, factor-oriented strategies by slowing down the convergence of mispricings. These results are consistent with a view that the rise of passive largely represents a “dumbing down” of investment activity in a way that might exacerbate mispricings but also increase their persistence. They are not consistent with a hypothesis that passive represents a diversion of assets away from unsophisticated investors who were actually exacerbating inefficiencies, which, if true, might represent a threat to the active opportunity set. The results also suggest that the impacts of passive are limited for scalable, lower-frequency investment processes, like Acadian’s. Impacts appear more pronounced for “faster” signals that generate higher turnover.

How Might Passive Affect Active?

Passive’s impact on the performance of quantitative signals should depend on the source and nature of passive flows. One possibility would be that the rise of passive reflects a shift of AUM away from investing approaches that are sensitive to fundamentals and help to prevent or correct mispricings. If so, then we might expect passive’s growth to increase the number and degree of mispricings and to expand the opportunity set for active investors who remain. But the impact on the efficacy of quantitative signals wouldn’t be clear. If convergence of mispricings to fundamental value were unaffected by the trend, then signal efficacy might remain unchanged. But if an increase in fundamentally insensitive flows and a reduction of capital allocated to harvesting inefficiencies delayed the correction of mispricings, then we might see reduced short-term efficacy of fundamentally based quantitative signals.

A second possibility is that the growth of passive represents a reallocation of assets away from naive forms of active investing that were actually exacerbating market inefficiency. That might reduce the opportunity set for more sophisticated active investors and diminish the efficacy of quantitative signals, even over longer horizons.

Testing The Alternatives

Ideally, we’d be able to evaluate passive’s impact by comparing the efficacy of quantitative signals in otherwise identical markets with disparate levels of passive investing. That’s not possible, of course. As an alternative, most discussions around the topic try to associate the gradual time trend in aggregate passive flows or market share with various effects. But such analyses have poor ability to discern impacts of passive investing’s growth. They have, in effect, only a few data points from which to draw inferences, and it’s difficult to isolate passive’s effects from those of all kinds of other concurrent trends.

For our analysis, we instead exploit stock-level information on passive ownership, which greatly increases the amount of data that we can bring to bear in testing for its effects. But doing so is quite a departure from the ideal “controlled experiment” described above. Stocks differ with respect to many attributes that may be related to passive ownership, such as liquidity and market capitalization, so if we want to isolate the incremental impact of passive ownership on signal efficacy, then we must control for such characteristics. In the analyses that follow, we also control for certain technical and risk factors.1

As our measure of passive ownership, for each stock in a developed markets (DM) universe we calculate the fraction of market capitalization held by passive institutions as reflected in consolidated global holdings of mutual funds and institutional investment managers’ 13(f) filings as sourced from the Thomson Reuters Global Ownership OP database (TR). TR categorizes ownership as passive or active at the institutional rather than the fund or account level, which introduces noise into the estimates.2

Most discussions of passive’s market share focus on U.S.- domiciled mutual funds, because that data is most readily available. In our sample, which is broader, we find that roughly 65% of the passive holdings derives from 13(f) filings, while the remaining 35% comes from mutual fund reports. Our data primarily reflects holdings of investment managers based in North America and the U.K., with relatively sparse information from other regions.3

Figure 1 highlights the evolution of passive ownership levels among stocks since 1998, when the data starts to appear reliable. The chart suggests that by 2018 about 30% of the typical North American stock was owned by passive mutual funds and institutional managers.4 In our sample, we observe that by March 2018 roughly 80% of U.S. stocks had non-zero passive ownership, versus 52% in developed markets more broadly (including the U.S.).

January 1998 – March 2018. Source: Acadian based on data from Thomson Reuters Global Ownership OP database. Passive assets comprise consolidated holdings of global mutual funds and 13(f) reports by institutional investment managers classified as passive by Thomson Reuters. This hypothetical analysis is being provided for illustrative purposes only.

Results

Figure 2 highlights the ex-post efficacy of our bottom-up stock return forecasts across the DM and North American universes and the impact of passive ownership. The ex-ante alphas combine contributions from Acadian’s proprietary value, quality, growth, and technical factor groups. To clarify interpretations, we have simplified calculation of the alphas relative to our production models, basing the forecasts on a one-month investment horizon and omitting certain adjustments. As noted above, to better isolate the incremental impact of passive ownership, the regressions underlying the analysis include controls for a host of variables, including firm size, risk, liquidity, and technical attributes.

The table’s first column shows that in the cross-section of the DM universe from 1998-2018, an incremental 1% of forecasted alpha has been associated, on average, with a 1.07% increase in realized return over the following month. This is strong evidence of the short-run cross-sectional efficacy of our bottom-up forecasts. But the second row shows that this ex-post payoff to alpha diminishes somewhat as passive ownership increases.

Specifically, for a stock with passive ownership of one standard deviation above the mean, the ex-post return per 1% of forecasted alpha drops by 0.05%. Summarizing in relative terms, higher levels of passive ownership reduce ex-post alpha efficacy on the order of 5%.

Column 2 shows that passive’s impact appears to have strengthened over time, rising to roughly 9% in relative terms (0.08%/0.95%) over the past decade. Figure 3, which charts cumulative returns to alpha assuming varying degrees of passive ownership (blue: none; red: +1 std. dev.; grey: -1 std. dev.), shows that the effect became more pronounced following the GFC, a period of substantial growth in passive investing in North America, as shown in Figure 1.

Returning to Figure 2, columns 3 and 4 show that the short-term interaction effect appears more pronounced in North America, over the past decade reaching 20% on a relative basis (0.18%/0.91%). This might reflect higher overall levels of passive ownership or more complete reporting in North America. It might also reflect regional variation in the actual composition of what has been classified as “passive.”

Source: Acadian. In rows 1 and 2, bolded values indicate statistical significance at conventional levels. Regressions are square-root-market-cap weighted and include controls for size, liquidity, beta, technical factors (e.g., short interest, options-derived, and peer momentum signals), and interaction effects between alpha and market capitalization and liquidity. Please contact us for further details. This hypothetical analysis is being provided for illustrative purposes only. Forecasts are based on proprietary models. There can be no assurance that forecasts can be achieved. Past results are not indicative of future results. Every investment program has an opportunity for loss as well as profit.

January 1998 – March 2018. Source: Acadian. This hypothetical analysis is being provided for illustrative purposes only. Past results are not indicative of future results. Every investment program has an opportunity for loss as well as profit.

Source: Acadian. In columns 1 and 2, bolded values indicate statistical significance at conventional levels. Regression specifications are consistent with those described in Figure 3. Please contact us for further details. This hypothetical analysis is being provided for illustrative purposes only. Past results are not indicative of future results. Every investment program has an opportunity for loss as well as profit.

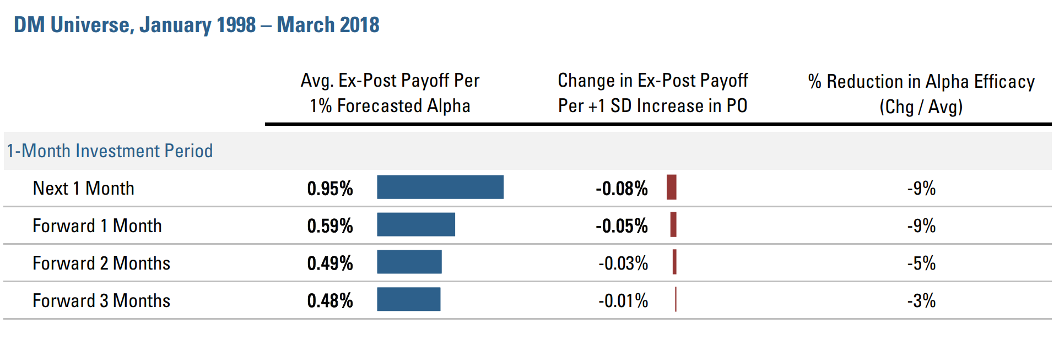

The competing hypotheses regarding the nature and sources of passive flows generate testable predictions regarding passive’s impact on alpha efficacy over different investment horizons. Figure 4 highlights results for the DM universe over the past 10 years, showing that the interaction becomes economically negligible and statistically insignificant when the investment horizon is pushed forward even just a few months. Specifically, while the alphas demonstrate considerable ability to predict returns in the cross section several months into the future (looking down column 1), passive’s impact on alpha efficacy diminishes fairly rapidly (columns 2 and 3). It is no longer statistically significant for 1 month returns, forward 2 months. Results for North America are broadly similar (unreported).

Source: Acadian. In columns 1 and 2, bolded values indicate statistical significance at conventional levels. Regression specifications are consistent with those described in Figure 3. Please contact us for further details. This hypothetical analysis is being provided for illustrative purposes only. Past results are not indicative of future results. Every investment program has an opportunity for loss as well as profit.

These results are inconsistent with the hypothesis that the rise of passive is improving market efficiency by diverting assets away from unsophisticated active investors that were exacerbating mispricings. If that were the case, we would expect persistent degradation of alpha efficacy, reflective of a reduction in mispricings. Instead, Figure 4 suggests that higher levels of passive ownership impede correction of mispricings in the short-run but have less effect over longer horizons. That would be consistent with passive investing delaying the incorporation of fundamentally relevant information into prices over relatively short horizons.

Figure 5 provides further evidence in favor of this interpretation, showing that passive ownership has greater impact on the efficacy of faster factors. Specifically, momentum and growth factors (e.g., analyst revisions, analyst recommendation changes, and earnings surprises) appear to be more negatively affected by higher levels of passive ownership than value and quality. The interaction of passive ownership with value isn’t statistically significant in either DM or North American universes over the full sample period or the past decade.

Conclusion

The results suggest that passive investing may be influencing the performance of active strategies. The picture that emerges favors a view that the rise of passive reflects a shift away from fundamentally informed investing that might even increase inefficiency but somewhat delay the correction of mispricings. That interpretation would be broadly consistent with empirical evidence that higher levels of indexation and ETF ownership reduce the information content of prices and that trading of ETFs generates non-fundamentally based demand shocks for the stocks that they hold.5

Pragmatically speaking, the impact of passive on forecast efficacy appears statistically relevant but modest, roughly similar to our bottom-up alphas’ interaction with market capitalization and trading volume. The results highlighting passive ownership’s relatively pronounced impact on faster factors suggest that the effects of the “rise of passive” may be smaller for fundamentally oriented, lower-frequency approaches like Acadian’s, than for technically focused, higher-frequency strategies.